Hamish McRae: US Inc is pretty chipper, but there will be a correction to the stock market before too long

Economic View: Don’t you love the way in the US people talk of earnings, whereas we here talk of profits?

For free real time breaking news alerts sent straight to your inbox sign up to our breaking news emails

Sign up to our free breaking news emails

The American economy is on the move again. The ground lost in the first quarter, when dreadful weather helped push it into retreat, has been more than recovered. The first quarter was not as bad as previously thought and the second much better than expected. The question now is whether the US locomotive continues to pull the rest of the world along the next stage of the recovery.

The central point here is that the US remains the world’s largest economy. It led the world into recession and it led it out. It is also Britain’s biggest export market, taking 14 per cent of our merchandise exports and 20 per cent of our service exports – though if you add together all the eurozone countries they are larger, taking 47 per cent and 34 per cent respectively. For all the emphasis on the Brics, and for all the importance to the UK of a eurozone recovery, the US still matters massively.

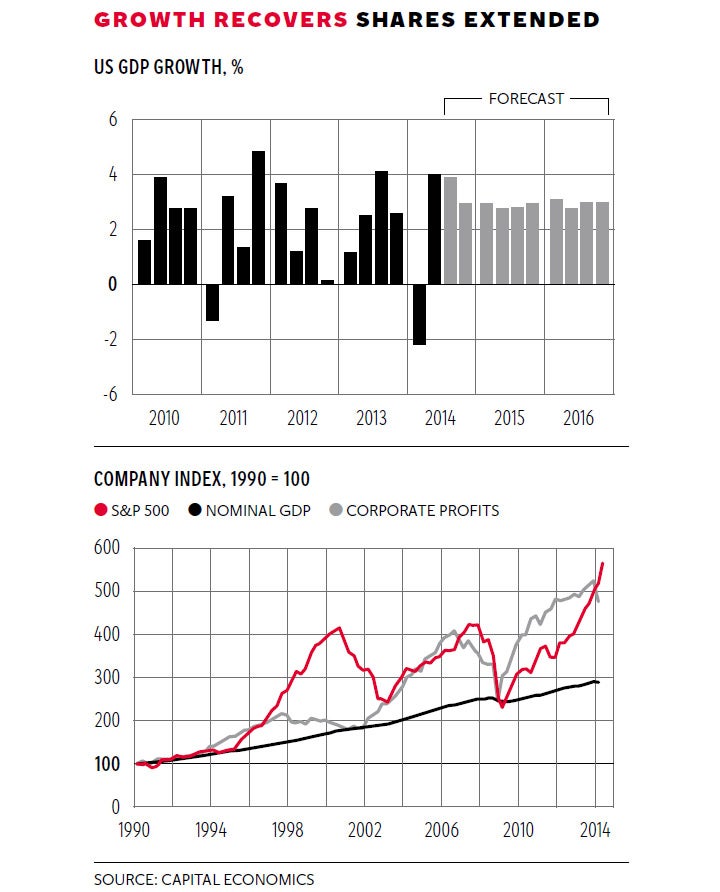

The GDP figures look backwards and will in any case be revised, as they always are. Looking forward, what can we say? The question is not whether there is another US recession around the corner (or at least there is really only one foreseeable set of circumstances where that might occur), but whether the economy continues at a 3 per cent annual clip for the next couple of years or slithers back to sub-standard growth.

The top graph shows the consensus outlook, a forecast from Capital Economics of the 3 per cent norm continuing through to the end of 2016. It will not be as smooth as that, and if you look at the past three years you would expect some bumps, but an aggregate 3 per cent growth outcome seems pretty sensible. It is what the economy ought to be able to sustain.

The latest forward-looking data supports this. Consumer confidence is exceptionally strong. Consumers say they think this is a good time to buy large-ticket items, and this is supported by the fact that cars and light truck sales are running at an annual rate of 17 million, the average level in the boom years to 2007. This is supported by a reasonable job market, with job growth running at or above 200,000 a month for the past six months. This is consistent with the fact that business confidence is very strong, with large businesses particularly so. This points to even faster growth, around the 4 per cent achieved in the second quarter, and while we are still only about a third of the way through the company reporting season, outcomes are currently better than market estimates in about two-thirds of cases. US Inc is pretty chipper.

The housing market is chipper too. It would be wrong to characterise the recovery as a housing-led boom, but there is a parallel with the UK, for ultra-cheap money has not only turned round the market in most places. It has also enabled existing home-owners to cut their mortgage costs, and the wiser ones are using the headroom to top up their pensions.

Whenever you go to a country you are always struck by things you could not have known had you not been there, and the surprise for me on a recent visit was the emphasis that people were putting on their pension planning. That may be a function of the strong stock market, or a hangover from the searing experience of recession, or simply a shift towards caution more generally. But anyway, pension planning is a hot subject in the media and in family conversations.

The most obvious measure of confidence about the future of the economy is the stock market, and you can see in the second graph how the S&P 500 has now far surpassed its previous two peaks. It is supported by strong earnings – don’t you love the way in the US people talk of earnings, whereas we here talk of profits?

But that graph carries a warning. Note that while share prices are more or less consistent with company earnings, both earnings and prices are way ahead of the trend in money GDP. That does not mean that share prices are “irrationally exuberant”, the expression coined by Alan Greenspan, former chairman of the Federal Reserve. There are plenty of rational arguments to support this level. But they are undoubtedly exuberant, which has led many to question quite how long such exuberance can continue. Pessimists argue that higher interest rates will puncture the stock market bubble. Optimists say it isn’t a bubble, just a reasoned response to a positive outlook. Put it this way: if that growth performance shown in the top graph proves more or less right, then share prices don’t look over-optimistic.

The problem with all this analysis is that the US in particular, and the developed world in general, has no experience of how to return to normal monetary conditions. We have never done it before, because the only previous periods of such low interest rates have been during and immediately after the Second World War. There was strong post-war growth in both the US and UK but much of this was catch-up, and the inflationary pressures that you might have expected to be generated by ultra-cheap money were contained, at least initially, by price controls.

I think what we can assume is that the Federal Reserve will be sensible. The US will be prepared for the rise in rates as and when it comes, just as it has been prepared for the tapering down of the monthly purchases of Treasury securities. Monetary tightening, at a measured and orderly pace, is so-to-speak “in the market”. There was nothing in the Fed statement yesterday that suggests otherwise.

If this is right, what can we expect? My best guess will be that there are another four or five years of decent growth, but with some bumps on the way, before there is a danger of a serious recession. But there will be another stock market correction long before that. Normality is not a never-ending bull market.

Subscribe to Independent Premium to bookmark this article

Want to bookmark your favourite articles and stories to read or reference later? Start your Independent Premium subscription today.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies