The truth about insolvency and your financial future

Are we kidding ourselves about the long-term consequences?

For free real time breaking news alerts sent straight to your inbox sign up to our breaking news emails

Sign up to our free breaking news emails

The average household debt is creeping towards £59,000.

Per adult, the typical amount we owe is increasing by almost £900 a year.

And when the credit runs out or the repayments fail, the house of cards can quickly come crashing down.

Figures out last week show the number of personal insolvencies has reached a seven-year peak. Individual voluntary agreements or IVAs are at a record high.

With bankruptcy numbers up almost 10 per cent in 2018, The Money Charity estimates someone in the UK is declared insolvent or bankrupt every five minutes.

With real wages still well below pre-financial crisis levels and household budgets stretched, the number of people who have reached the end of the debt repayment road is expected to stay high.

“We expect insolvencies to remain at this high rate throughout 2019 and 2020, fuelled by high consumer lending and the forceful marketing of companies offering personal insolvency as a debt management solution,” notes Richard Haymes, head of financial difficulties at TDX Group, an Equifax company.

“It is a worry to see the number of people going insolvent at its highest level for seven years and this reflects the challenging times many people continue to face.

“With this increase [in the number of people going insolvent] driven in large part by a rise in IVAs our concern is that many people in debt are being led down a route that may not be suitable for their circumstances,” says Joanna Elson, chief executive of the Money Advice Trust, the charity that runs National Debtline.

“The prevalence of online adverts that promote ‘solutions’ to debt involving insolvency procedures may well be a contributing factor to this.”

But debt management solutions mean different things to different people and insolvency doesn’t just mean bankruptcy. Confused? Millions of us are. And yet despite the best efforts of breezy, instant-fix marketing messages touted by any number of debt management firms, the decisions we make about how to deal with our ever increasing debt can have long-term consequences we hadn’t even thought of.

What’s in a name?

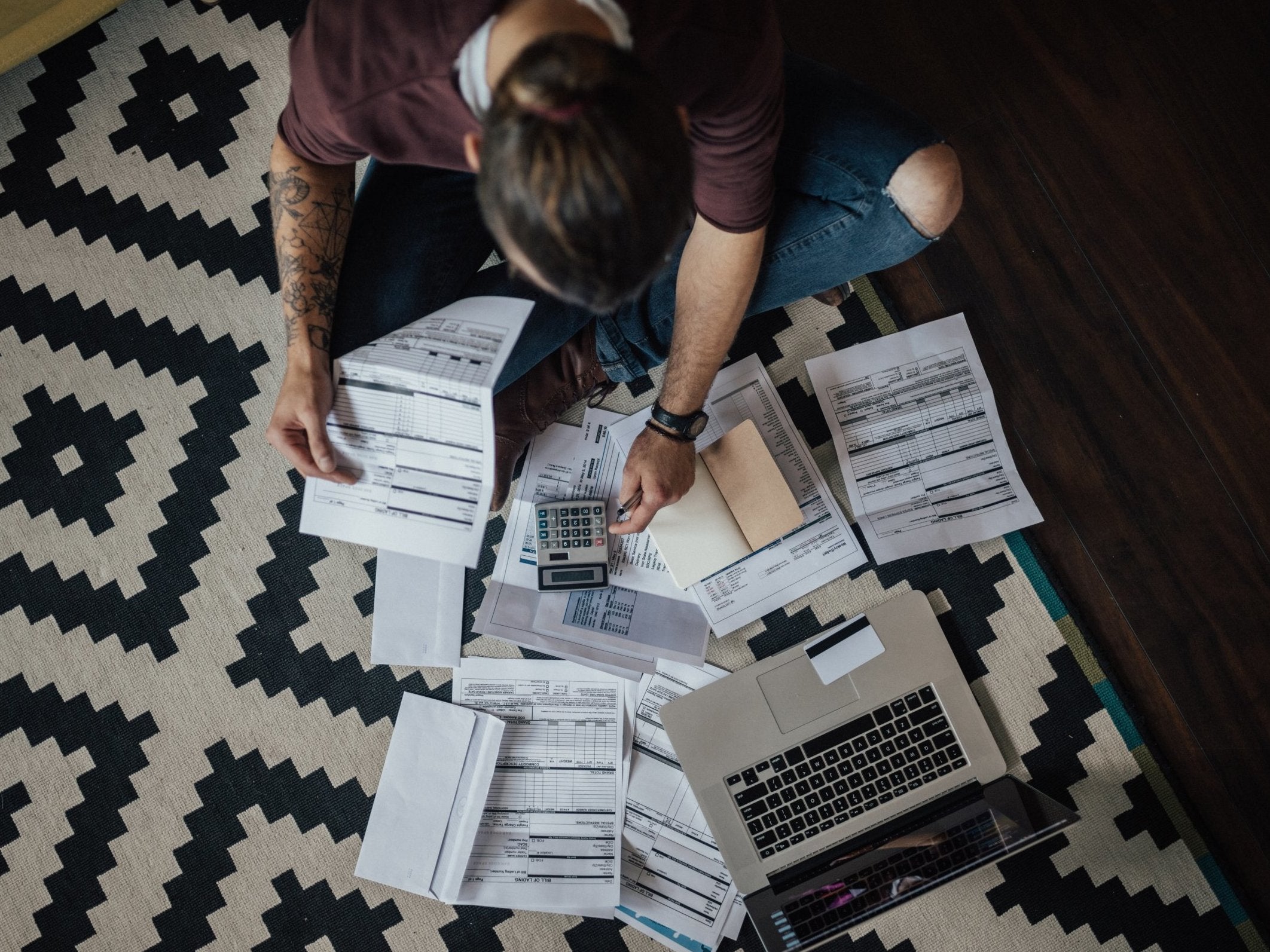

You’ve got debts, unwieldy, growing debts that leave you sleepless for fear that the lights are going to go out. You’ve done your best to manage your spending better and pay your creditors off. But you just can’t make ends meet. You may be falling behind with even the minimum payments.

Most people don’t seek help with this so-called “problem debt” early enough. When they do, ideally by contacting an impartial debt charity, the first step is to create a budget, cut down costs as far as possible and give full repayment your best shot.

A debt management plan is an agreement you and your creditors make to pay off your debts – usually because you can only afford to repay a very small amount each month. You can do it yourself, via a charity or through a fee-charging debt management firm (an administration order is a similar way of paying debts if you have a county or High Court judgment against you of less than £5,000 and can’t pay in full).

Sometimes the numbers just won’t add up though.

Then you really have two options as a UK-based individual – an IVA to pay some of the debt back at least or bankruptcy. And depending on who you speak to these are either dreadful no-other-choice obligations that will stop you getting more than a paper round for the rest of your life or an easy way to wriggle out of a financial headache whose consequences won’t really matter in a year or two.

“[There are] major misperceptions around the consequences of personal insolvency,” warns Haymes. “Nearly three in 10 people don’t realise that entering personal insolvency could affect their access to rental accommodation, over a quarter of people don’t know it may affect their eligibility for a bank account, and nearly one in five Brits think it wouldn’t influence their ability to access a mortgage.

“Our research shows people don’t realise the impact on their access to other everyday services. For example three in five Brits believe there would be no issues in accessing utility services such as electricity, gas, or TV and broadband services.

“There’s wholesale confusion concerning the consequences of personal insolvency. Entering into an IVA is recorded on your credit report for six years and can make it hard for you to be approved for rental agreements, a mortgage or bank account, as well as other services like utilities. It’s never a decision to be taken lightly.

“While an IVA serves a valuable purpose when someone’s financial situation has spiralled out of control, we urge anyone experiencing financial pressure to seek help from their creditors or free independent money advice at an early stage so alternative solutions can be explored.

“The government consultation on increased breathing space and the statutory debt repayment plan closed this week, and is designed to provide more support for consumers. The more we publically debate debt and ways to manage it, the better the outcomes will be for individuals, businesses and the economy as a whole.”

National Debtline offers free, independent and confidential debt advice.

Subscribe to Independent Premium to bookmark this article

Want to bookmark your favourite articles and stories to read or reference later? Start your Independent Premium subscription today.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies